The Disconnect Between Oil Futures and Fuel Prices

Despite easing geopolitical tensions, gasoline prices remain high while oil prices fall. Markets are pricing in calm, but consumers are still paying the fuel costs of the crisis, around $4-$6 per gallon, depending on the state.

Since the United States and Israel attacked Iran on February 28th, Tehran has effectively restricted flows through the Strait of Hormuz, one of the world’s busiest oil shipping routes. About 20% of global oil passes through the strait, leading to a significant increase in global oil prices. In 2025, approximately 20 million barrels of oil and oil products passed through the Strait of Hormuz per day, according to the U.S. Energy Information Administration (EIA). The Iran conflict and the disruption of the strait have triggered what the International Energy Agency (IEA) has described as one of the largest supply disruptions in the history of the global oil market.

After a month and a half of conflict in the Middle East, President Donald Trump announced a two-week ceasefire last Tuesday. Oil futures responded almost instantly to the announcement. However, physical supply routes remain under pressure. As Tom Kloza, chief energy adviser at Gulf Oil, explained, “The physical disruption is real and peoplere frustrated because the futures market is kind of orderly and calm.”

Traders interpreted the ceasefire as a reduction in geopolitical risk pushing oil futures prices lower. Oil futures prices reflect what traders expect oil to cost in the future, not what it costs physically today. Gasoline prices, by contrast, reflect the replacement cost of physical inventory. They take into account what it costs refiners and distributors to secure, process and deliver barrels of crude oil through a complex supply chain that is being affected by the conflict.

The divergence between oil and gasoline prices can be explained by the constraints of the physical energy system. Refineries behave as bottlenecks, they have fixed capacity and operating constraints, therefore even though crude oil price changes rapidly it takes time to pass into gasoline output. Furthermore, there is a physical supply chain lag, so shipments already in transit and existing contracts still reflect previous higher costs. Another factor affecting this price difference is war-risk premiums, which adjust more slowly than future markets.

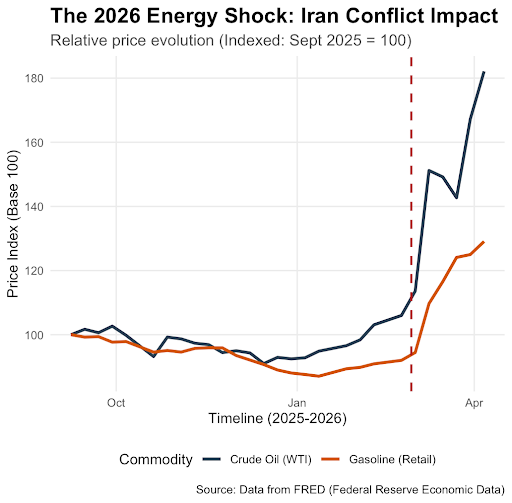

To illustrate this dynamic, I have created this graph showing the relationship between crude oil prices and gasoline prices using data from FRED. The data reveals two distinct market behaviours. Crude oil futures experienced a vertical spike following the outbreak of the conflict at the end of February 2026. Oil behaves as financial assets and they react instantly to geopolitical risk and anticipated closure of the Strait of Hormuz. On the other hand, gasoline prices follow a smoother trajectory. This time lag is caused by fixed costs of refining and transport. This reflects how oil markets are driven by expectations, whereas gasoline prices are shaped by physical processes.

Ultimately, the disconnect between oil and gasoline prices reveals a deeper reality: energy markets no longer move as a single system. Oil prices respond to expectations, but gasoline prices reflect the constraints of the physical world. In times of geopolitical uncertainty, it is this slower, more rigid system that determines what consumers pay.

Graph depicting the relationship between crude oil prices and gasoline prices.